Peak West?

There has been striking coherence in the Western-led response to Russia’s invasion of Ukraine. Economic sanctions on Russia and military/financial support for Ukraine have been consistent across the West (and friends); NATO is being expanded and strengthened; and there has been a collective stiffening of the Western spine with respect to China, from technology to Taiwan.

Countries have been making sharper choices on alignment. However, the emerging world will be messier than a binary framing of a Western-led bloc and a China-led bloc. A multipolar world of overlapping blocs is more likely.

Indeed, recent political developments in the US and elsewhere suggest limits on the coherence of the West. It may be that 2022 is the high water mark of the West: ‘peak West’.

America First

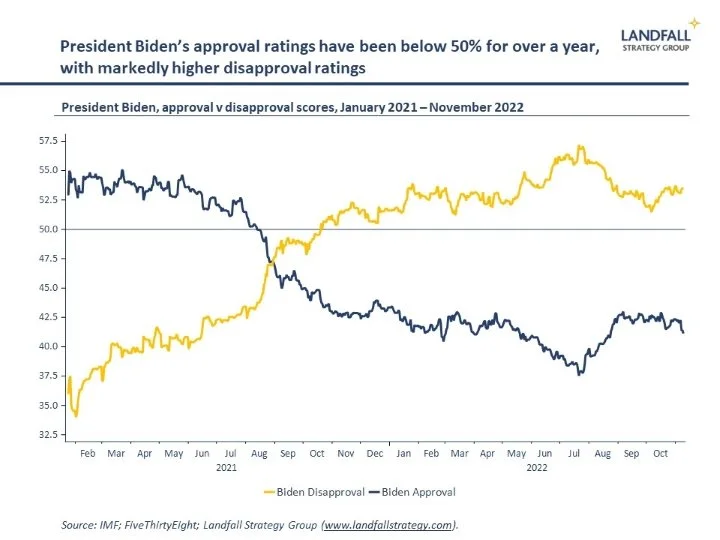

This week’s US mid-term elections saw a better than expected showing for the Democrats, and a bad night for Mr Trump’s MAGA wing of the GOP. I continue to think Mr Trump won’t run again; and certainly that he won’t secure the Republican nomination. But although two years is a very long time in politics, and the polls overstated Republican strength this week, the available polling – and Mr Biden’s low popularity – suggests that a Republican Presidential candidate is odds-on to win in 2024.

But to the rest of the world, broad continuity is likely either way. The inward turn of the US over the past several years is structural, not restricted to a particular Administration. Indeed, there has been much external and economic policy consistency between the Trump and Biden Administrations, despite the calmer behaviour and rhetoric. There is bipartisan support for a more disciplined version of the Trump Administration’s America First agenda.

Faultlines emerging

There are at least three areas in which this policy trajectory is creating stresses across the West.

First, US industrial policy activism has crossed the line into protectionism, with sweeping local content requirements (semiconductors, electric vehicles, and other green technologies). Provisions in the Inflation Reduction Act and the Chips and Science Act disadvantage non-US firms.

This is creating pushback from European countries as well as in Asia (Japan, South Korea) whose firms have built positions of competitive strength in these areas. President Macron has proposed a Buy European Act; and there are discussions underway about more aggressive European industrial policy in response. A form of trade war is increasingly possible (or perhaps a subsidy war).

High-level discussions are underway between the US and the EU, but domestic US politics makes meaningful progress unlikely.

Second, the hawkish US stance on China will continue to escalate – with gaps increasingly emerging on China policy between the US and others. For example, the US has imposed sweeping economic sanctions and restrictions on China (most recently on semiconductors), and is now pressuring other countries to move in this direction (from the Netherlands to South Korea).

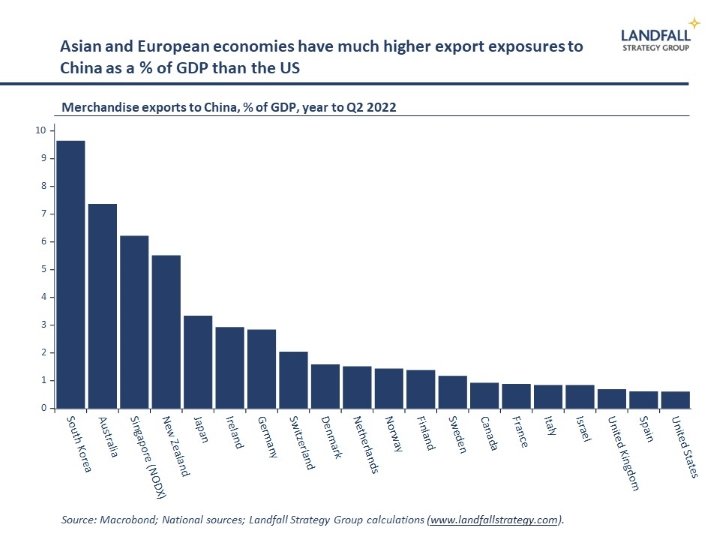

An increasingly hardline US stance on China, which requires more of its partners, will create frictions between the US and others. Although many Western-affiliated countries in Europe and Asia have toughened their policies and rhetoric on China, and public opinion is hardening, there is anxiety about full decoupling. The much higher levels of economic exposure to China in Asia and Europe explains why their hawkishness on China is less ‘full spectrum’ than the US (‘follow the money’).

Although an outlier example, Chancellor Scholz met with President Xi in Beijing last week, accompanied by a large German business delegation, having just signed off on a Chinese acquisition of a port facility in Hamburg. Mr Scholz has said that decoupling is not an option. This is essentially a continuation of Ms Merkel’s policy settings (although this week, Germany rejected a proposed Chinese acquisition of a semiconductor firm). But more broadly, there is daylight between the US and Europe on China.

And many Asian countries are cautious about signing on to US sanctions on China, particularly when the US continues to show no appetite for opening its markets to Asian firms. Indeed, Singapore signed 19 deals with China this week. And in a very interesting speech on Wednesday, Singapore’s Foreign Minister floated the idea of a ‘non-aligned movement’ in science, technology, and supply chains to avoid the ‘abyss’ of bifurcation.

Third, there is an increasingly ‘America First’ stance, with less support for allies and partners (or ‘entangling alliances’). For example, differences on support for Ukraine are already evident across Republican leadership. I expect ongoing US support for Ukraine, but this will be more contested. This matters because the US is – by a very substantial margin – the major provider of support.

There has been sustained nervousness across Asia and Europe on the reliability of the US. The willingness of the US to commit to its allies – particularly in economic terms – has been limited: it withdrew from TPP and has not been prepared to offer market access. And this is likely to weaken further after the Biden Administration. As a result, Western-affiliated countries with large economic exposures to China are looking to keep options open where they can. Although of course, hedging in this way is not always possible (or cost free).

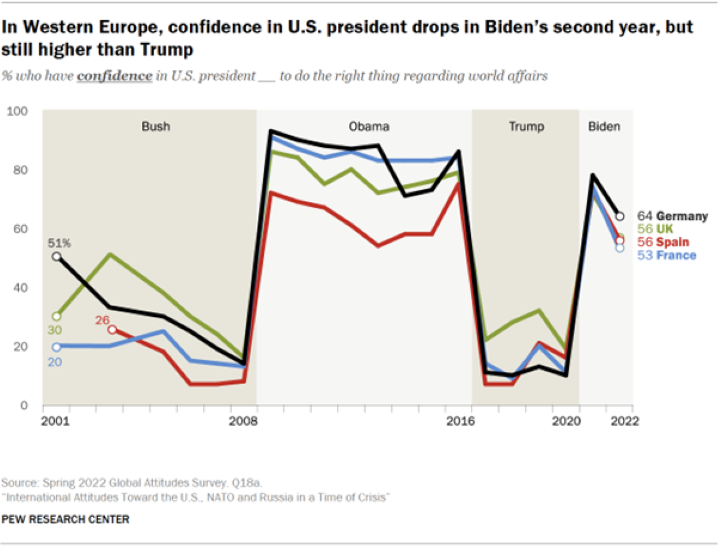

Attitudes towards US leadership across many advanced economies have recovered through the Biden Administration, but remain lower than a decade ago – and are vulnerable to another reduction.

Peak China also

However, China may not be able to take advantage of reduced Western coherence. Alongside the fractures across the West, there are increasingly evident weaknesses and contradictions in China. China’s growth potential – and its ability to project economic and geopolitical power – is running into constraints. Its ability to overtake the US as the world’s largest economy is not certain.

As I noted recently, China’s growth is slowing both in the near-term (Covid lockdowns, property markets) and structurally (capital misallocation, high debt levels, a shrinking working age population). And Western sanctions will constrain its growth potential. China is also an increasingly closed economy, and is actively reducing exposures to the West. The current leadership is focused on security and political goals rather than on economic objectives.

China will continue to be a dominant part of the Asia Pacific economy, and a key market for many economies. But its global dominance is not assured. And although its transactional diplomacy is attractive to some, its ability to develop deep and broad relationships is limited (and some of its friends, like Russia, are not in good shape).

A multipolar world

The fragmenting global economic and political system is likely to be a complicated, multipolar world with overlapping groupings – open for some purposes, closed for others. We should not take the Western coherence seen in the first half of 2022 for granted.

Of course, there are strong shared interests and values across the Western grouping – evidenced in the response to the Russian invasion of Ukraine. Another similar crisis – perhaps most obviously, a Chinese invasion of Taiwan – would also likely strengthen the Western grouping. But without such an existential crisis, the differences in posture are likely to lead to increasingly obvious faultlines.

Countries will increasingly be required to make choices on strategic positioning and alignment. But geography shapes the options and incentives facing countries, and we should expect a more regionally organised global economic and political system. In a world where geography is back, ‘vertical alignment’ (longitudes) will matter more than ‘horizontal alignment’ (latitudes).

In the real world, all politics is local. But the West – and particularly the US – needs to take care that domestic politics takes relations with its allies and partners seriously; and that it does not undermine the coalition supporting the rules-based system. Particularly for small economies, there are risks - and these dynamics require careful watching and thought.

If you are not subscribed yet and would like to receive these small world notes directly by email, you can subscribe here:

We provide insights and advisory services to firms, investors, and governments on responding to global economic and geopolitical dynamics. Please do get in touch with me at contact@landfallstrategy.com if you would like to discuss how we can support you.

Chart of the week

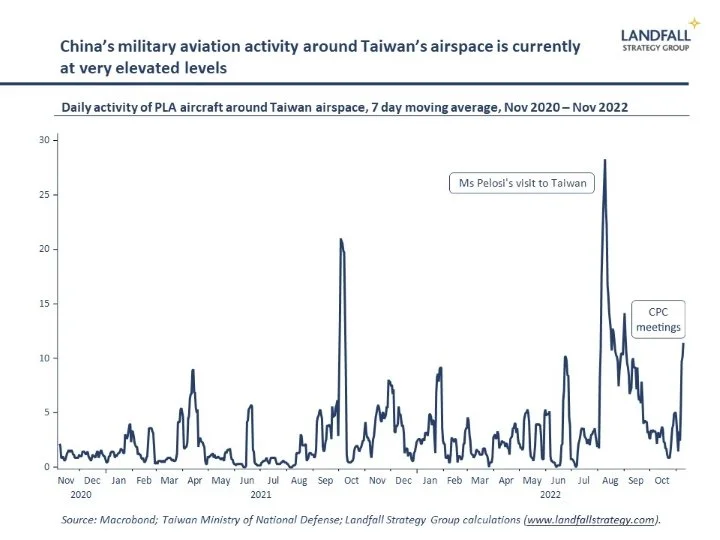

China’s military aviation activity around Taiwan has stepped up again after the Communist Party meetings in October. It is at levels only seen a few times over the past two years, only below the spikes in China’s incursions after Ms Pelosi’s visit to Taiwan in August and the tensions a year ago (after Taiwan’s application to join the CPTPP, among other things). This activity has become unfortunately normalised, but it is a reminder of the elevated risk profile across the Taiwan Straits.

Dr David Skilling

Director, Landfall Strategy Group

www.landfallstrategy.com

https://davidskilling.substack.com