From the market state to state capitalism

My writing regularly references ‘regime change’. So in this note, I outline my assessment of the characteristics and implications of this global economic and geopolitical regime change. I provide insights on these issues in advisory work as well as client briefings, online or in-person in London, Singapore, and beyond.

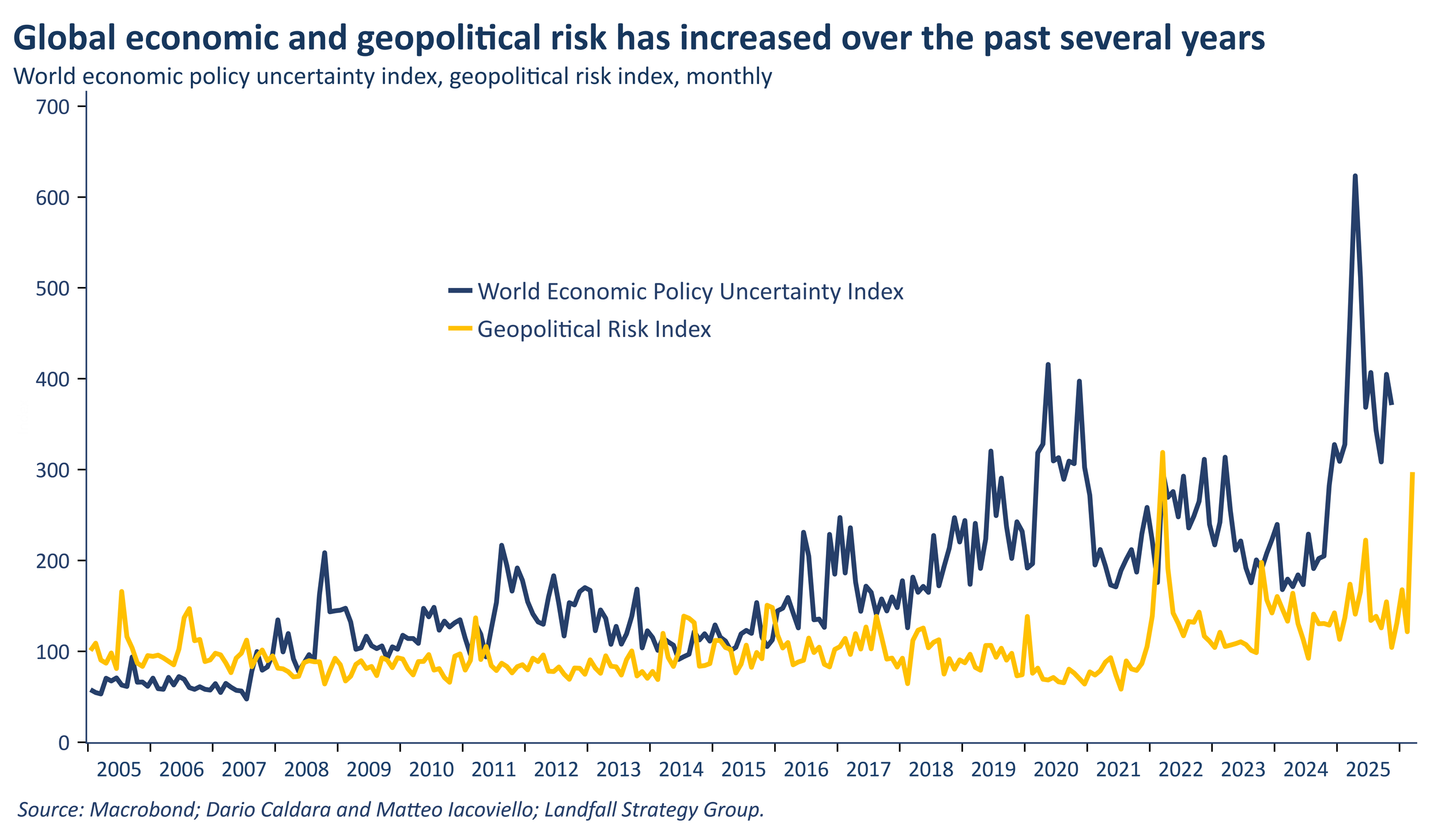

There has been substantial economic and geopolitical disruption over the past few years. As just a few examples: the Russian invasion of Ukraine in 2022; Liberation Day tariffs and a reset of US international engagement; the second China shock; the current Middle East conflict; rapidly increasing investments in security and strategic autonomy; a surge in gold prices and a sell-off in the USD.

A key judgement to make is whether this is a discrete period of elevated volatility that will fade or mean-revert over time, or whether this reflects a deeper shift in the organising logic of the global economy. My assessment is that structural regime change is underway. The status quo in domestic policy, and in international economic and geopolitical arrangements, is no longer sustainable. There is an underlying logic to this structural change that extends well beyond the effects of the Trump Administration or other temporary factors.

Since the end of the Cold War, the global economy has been organised around what I call the market state. Across most advanced economies, this meant the Washington Consensus (broadly speaking) in terms of domestic policy: fiscal discipline, central bank independence, and a relatively constrained, neutral role for government. Abroad, it meant a process of deepening economic integration; and largely on commercial rather than geopolitical terms. The market state prioritised efficiency, openness, and a non-activist state.

Firms and investors, and many countries, have prospered in this world. But disruption and turbulence over the past several years is a sign of profound change in the global economic and geopolitical system.

The market state regime has been weakening. In its place, a state capitalism regime is emerging in which governments actively shape domestic and international markets to secure economic, technological, and strategic advantage. The state is deliberate, discretionary, and takes power seriously. Economic policy is embedded in national strategic goals, not the other way around.

Structural drivers of change

This regime change is a response to three structural dynamics.

First, geopolitical rivalry has returned as a first-order force shaping the global economy. This is not simply military competition, but full-spectrum geopolitical rivalry involving strategic economic competition over technology, industrial capacity, energy, and more. The post-1990 default assumption was that global engagement was almost always shaped by commercial factors. But trade, capital, and technology flows are now importantly shaped by geopolitical competition. There is much greater sensitivity to dependency, vulnerability, and ‘hold-up’ risk.

Second, domestic political economy pressures are forcing changes in the economic policy mix across advanced economies. The Global Financial Crisis was a major point of rupture, with weak productivity growth, distributional issues, and recent inflation further undermining confidence. The rise of populism in many advanced economies reshapes the economic policies that are possible.

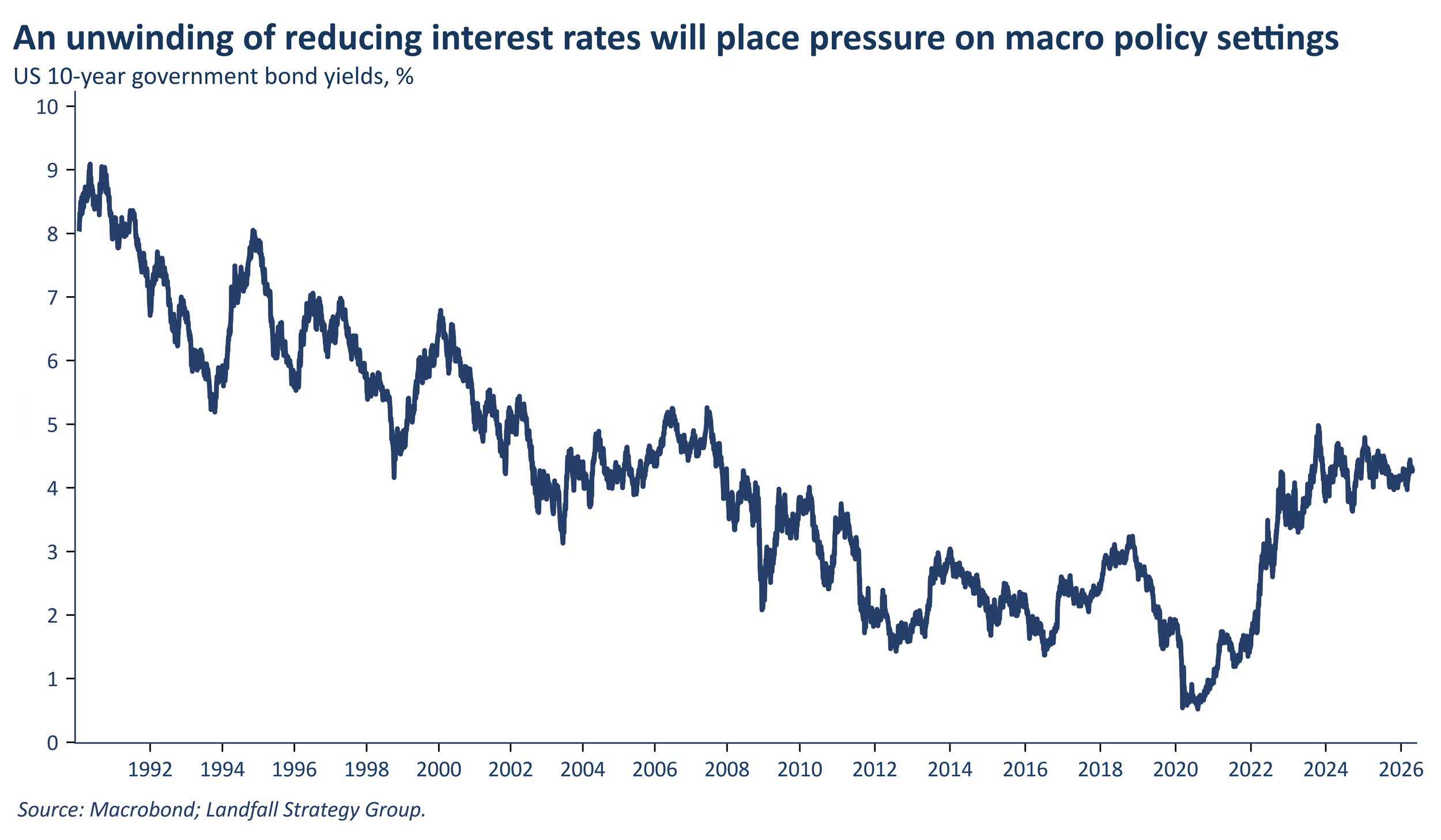

Third, macro policy is under pressure from emerging strategic imperatives. Public debt is already at record peacetime levels in many advanced economies, and will likely increase further on policy demands (military spending, industrial policy), political constraints, and higher interest rates. The fiscal and monetary orthodoxy of the past three decades is in tension with what governments need to do in this new economic and geopolitical context.

Toward state capitalism

Taken together, these forces are driving an accelerating shift from the market state towards state capitalism. The next decade will look materially different from the post–Cold War period, as the market state gives way.

There are several defining characteristics of state capitalism. There will be a greater reliance on policy discretion rather than technocratic rules (fiscal rules, central bank independence); economic strength (supply chain resilience, strategic autonomy, the ability to withstand coercion) will become more central relative to efficiency goals; and international commerce will increasingly be approached as zero sum rather than as a series of mutually beneficial transactions.

Regime change will play out across three core domains.

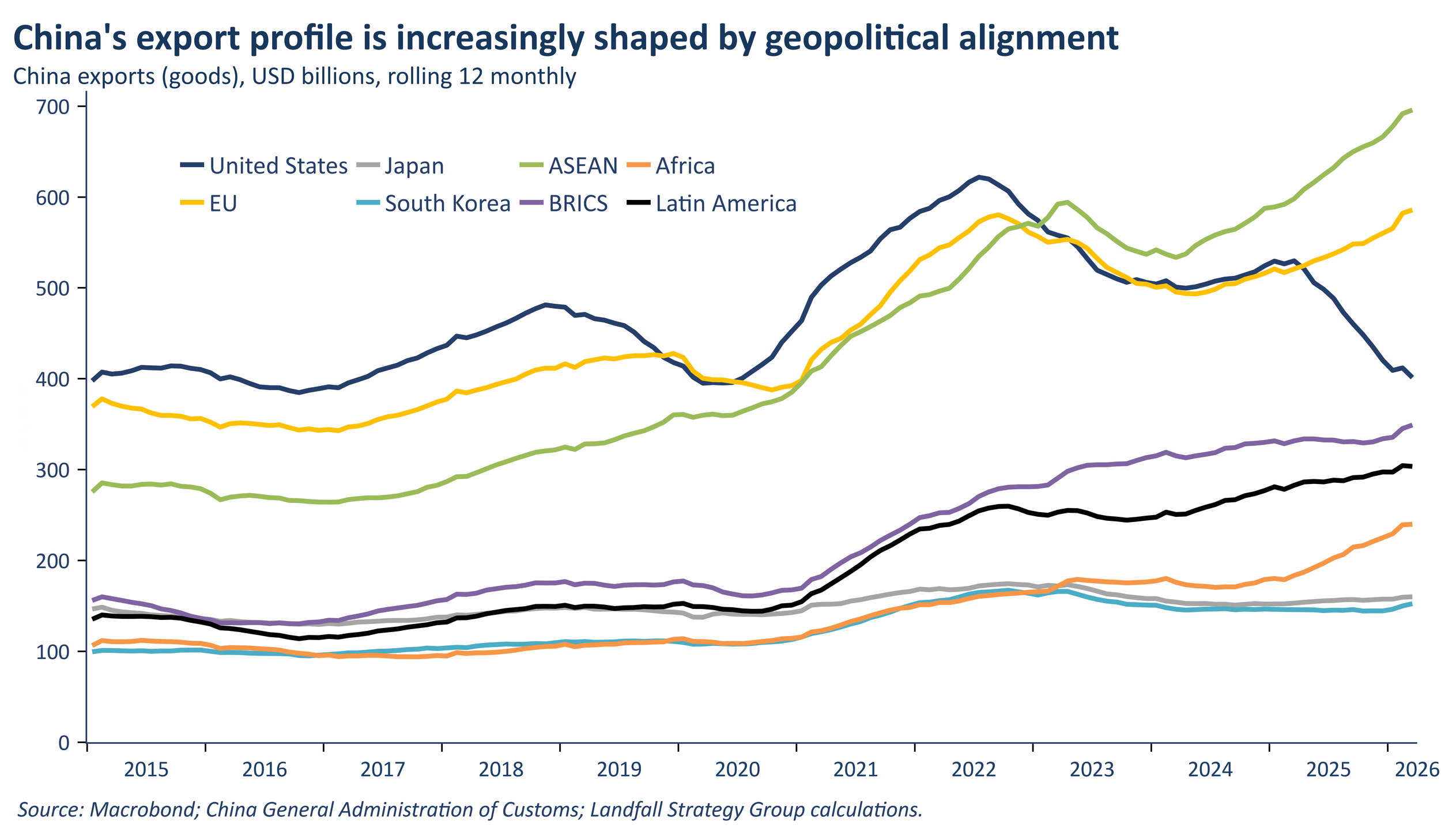

Global economic strategy. Globalisation is unlikely to unwind, but it is being rewired. Trade and capital flows will increasingly be shaped by geopolitical alignment as firms, investors, and countries reduce exposure to rivals and to unconstrained great powers. Supply chains will continue to reconfigure around security and resilience. Openness will no longer be the default, particularly in areas that matter for security or political stability. A more fragmented global economy is emerging.

Industrial and innovation policy. State capitalism places greater emphasis on building national advantage in strategically important sectors, such as defence and advanced technologies. This will involve material public support: direct subsidies and procurement, public investment in research ecosystems, policies designed to mobilise private capital towards strategic priorities, and support for national champions. Expect substantial increases in public and private sector investment: state capitalism will be more capital-intensive than the market state across advanced economies.

Macro policy. The greater spending and investment demands on government balance sheets, combined with political constraints on fiscal consolidation, implies ongoing debt accumulation in breach of existing fiscal rules. This also means that less capital will be exported by current account surplus countries, making it more difficult to finance public borrowing in current account deficit countries. In response, financial repression, fiscal dominance, and an erosion of central bank independence is likely in order to expand fiscal space. Looser monetary policy combined with strong domestic demand and frictions on global flows is likely to mean structurally higher inflation.

Because economic arrangements are downstream of the geopolitical order, an increasingly contested geopolitical order implies a more diversified, fragmented global economic and financial system. The US became increasingly central to global economic and financial arrangements during the market state era, reflecting US geopolitical dominance and because network effects made this the efficient solution.

The leading position of the US/USD will not be quickly displaced, but this regime change does imply a structural shift from the unusually unipolar moment of the post–Cold War period. Alternative nodes and groupings will deepen their own trade, investment, reserves and payments arrangements.

Our data-heavy monthly ‘Regime change tracker’ describes widespread, material, and coherent structural change across these multiple domains.

Costs, risks & opportunities

It is straightforward to identify the risks and costs of this regime change: more discretionary economic policy, higher trade frictions, and a weaker rules-based system. These are real. But state capitalism does not inevitably mean worse economic outcomes. Indeed, global GDP growth and world trade has been resilient despite the disruptions of the past year – at least prior to the Iran-related shock.

There are credible positive scenarios. Nominal GDP growth may be higher, supported by looser macro policy and large strategic investment programmes. And capital deepening across the economy, combined with increased investment in research and innovation may support a productivity renaissance; further supported by AI and other disruptive technologies.

Performance across countries is likely to vary substantially. The winners in the emerging regime will tend to share several features: strong state capacity to deliver active economic policy; robust national balance sheets to fund strategic investment at scale; political legitimacy to sustain long-term commitments; existing industrial, innovation, and technology capabilities; and meaningful strategic autonomy in energy, commodities, and technology. There is significant variation across countries on these dimensions, which means significant variation in outcomes.

My assessment is that there is unlikely to be a consistent pattern of increasing returns to economic scale. Small advanced economies with strong institutional capabilities and smart competitive positioning can continue to outperform larger economies.

Positioning for a new world

Firms and investors need to position for the structural challenges and opportunities presented by this regime change. For firms, international footprints and supply chains need to be assessed through a geopolitical lens; new sectoral and market opportunities will emerge; and balance sheets need to be managed for a context of elevated uncertainty. Investors need to position for a very different macro landscape (higher inflation, looser fiscal, new macro policy institutions), new patterns of capital flows, including more uneven sectoral returns, and a diversification away from US allocations.

Overall, the big risk is assuming that the past few decades provide a reliable map for the next decade and beyond. Firms, investors, and governments who internalise regime change, and position early for the new regime, are likely to be better placed than those who treat the recent economic and geopolitical turbulence as a temporary deviation.

I work with investors, corporate leadership teams, and governments, providing advice and briefings on the implications of global economic and geopolitical regime change.

Contact: david.skilling@landfallstrategy.com

To receive my free public notes on global economics & geopolitics, subscribe at: https://davidskilling.substack.com/