Iran & a new world economic order

This note draws on analysis prepared for Landfall Strategy Group clients. I discuss the implications of global economic and geopolitical regime change, including developments such as the Iran conflict, in client briefings and advisory work, both virtually and in person in London, Singapore, and across Europe.

There is significant uncertainty about the near-term military outlook in the Middle East, and the consequent economic and market impact. President Trump threatened to hit Iran ‘extremely hard’ over the next few weeks in his Wednesday night speech, after a series of public remarks that signalled a search for an offramp. This toggling between threats and deals is standard negotiating behaviour from Mr Trump.

Even if Mr Trump does reach some near-term resolution with Iran, there will not be a return to the status quo ante: risk and costs will persist, and it will take time to resume energy flows, even if Brent crude futures are pricing a significant unwinding of oil prices through 2026.

And this conflict will have enduring, structural economic and geopolitical effects. This note discusses five structural economic and geopolitical consequences

1. Energy independence/supply chain resilience

Firms and countries are dealing with the latest in a series of supply chain shocks (after Covid, Ukraine, Suez Canal) and will respond more aggressively to what is now understood to be a new normal of elevated risk to global supply chains.

First, increased investment in energy independence: from renewables and nuclear capacity to expanded production of domestic oil and gas. Second, countries will be diversifying energy suppliers where possible. Watch for new energy flows, even between countries with otherwise strained relations, particularly across Asia. Third, energy reserves will be rebuilt and likely expanded to respond to the higher global risk profile. This demand impulse will contribute to higher for longer energy prices.

2. Macro stress

High energy prices will create a drag on global economic activity, and likely worsen the effects of the second China shock in Europe and emerging markets.

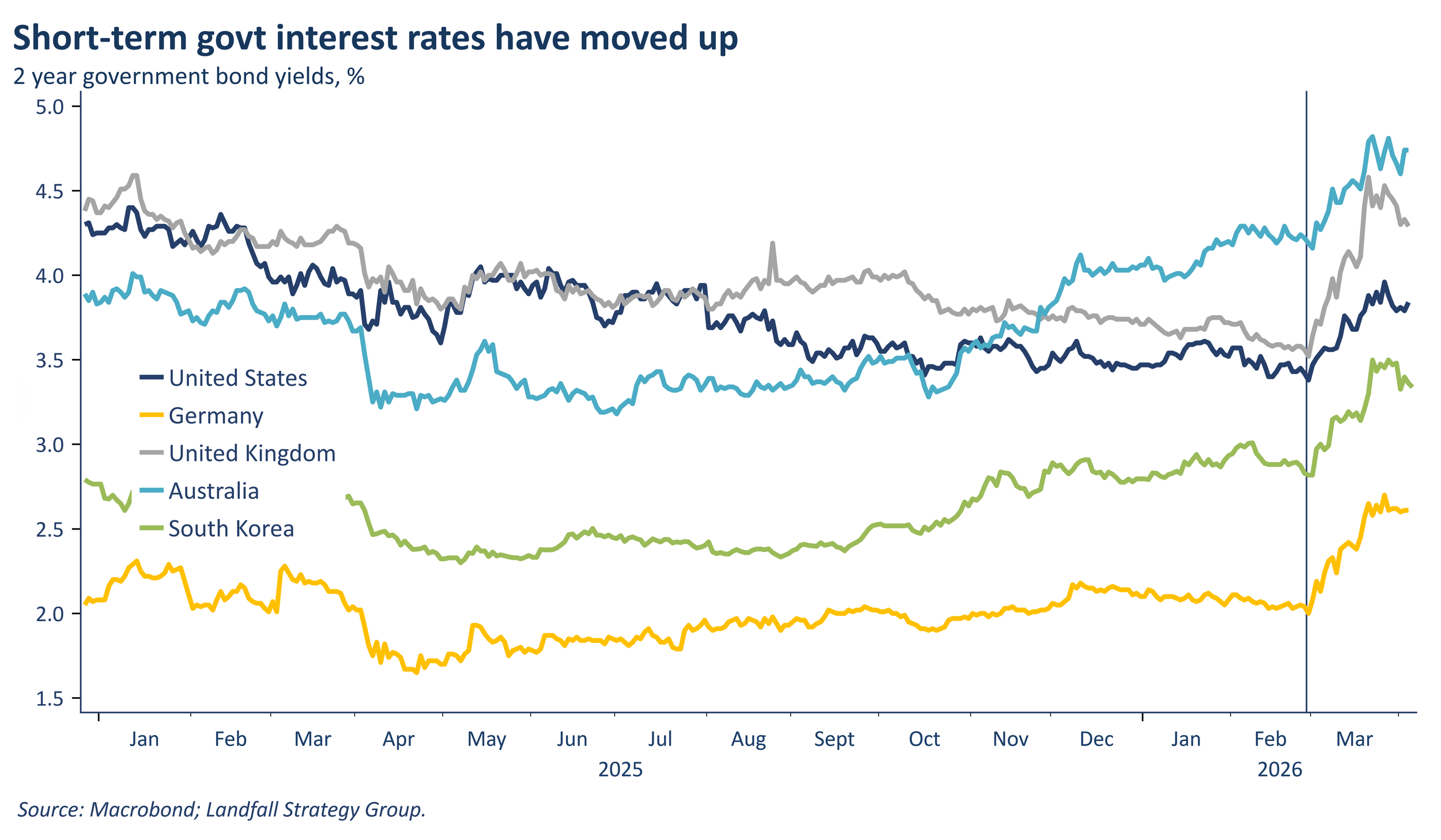

The conflict will also place additional stress on macro policy. Pre-war, inflation across advanced economies was persistently above target; public debt levels were at record peacetime highs; and the fiscal outlook was unsustainable.

My expectation is that inflation will be structurally higher as a broad range of input costs remain higher for longer as a consequence of the conflict, leading to enduring cost of capital pressures. The offset is that an economic shock may lead central banks to loosen monetary policy. However, this price shock combined with structural inflation pressures means that interest rates are more likely to remain higher.

The war will create additional fiscal pressures, with increased spending, debt servicing costs, and weaker tax revenues. Europe may be economically exposed to the conflict, but the US is particularly fiscally exposed (and note President Trump’s proposal last week for a 44% increase in annual defence spending, to $1.5 trillion in FY27).

3. Geopolitics v economics

Beyond these economic impacts, this conflict is also a deeply consequential geopolitical event. So it is striking that markets are pricing this almost exclusively as an economic shock: there is a tight correlation between daily movements in Brent crude prices and movement in equities and rates, with little evidence of geopolitically-driven pricing (cf. the Ukraine invasion in 2022) in terms of safe haven flows. It is priced as a textbook economic shock.

This market behaviour is consistent with a common view of geopolitics as a vector of risk events (shocks), with a short half-life from the perspective of market returns. But the more important geopolitical perspective on the Iran conflict is that it will reinforce and accelerate the structural geopolitical regime change underway to a more diversified, fragmented, contested global system. These economically meaningful geopolitical consequences will be increasingly recognised over time, in ways that differ sharply from the initial market reaction.

4. Geopolitical rupture

The US demonstrated its unrivalled hard power in the attacks on Iran. But this will have material geopolitical consequences in ways that are likely negative for the US.

The advantages of US military supremacy are offset by the unpredictability of the use of this hard power and erratic US decision-making. There was no consultation with allies on Iran, or any meaningful consideration of their economic and security interests. In response, US partners in Europe, Asia, and the Gulf will likely diversify partners and invest more in security and other capabilities in order to reduce exposure to the US. The US attack on Iran reinforces the experience of the past year (Greenland, Ukraine, NATO, Liberation Day tariffs, and more), suggesting that the US is an unpredictable, unilateral, transactional, revisionist power.

The second vector of geopolitical change is in terms of a transfer of geopolitical power. There is much uncertainty here, but there is a growing likelihood that the US leaves the conflict without full control of the Strait of Hormuz being achieved. This retreat from the 1980 Carter Doctrine would be a major loss of US credibility. It would also highlight the exposure of the US to physical chokepoints, a major issue for Asian security. The dominance of the US has been eroded because of its strategic errors around the Iran conflict. China is advantaged by default.

5. Capital flows & USD centrality

US economic and market exceptionalism since the global financial crisis, and over longer time periods, has been importantly based on its ability to mobilise foreign capital. These capital flows, and accompanying exchange rate arrangements, are downstream of US-centred geopolitical arrangements. A more diversified, multipolar system will emerge, which will have material implications for capital flows.

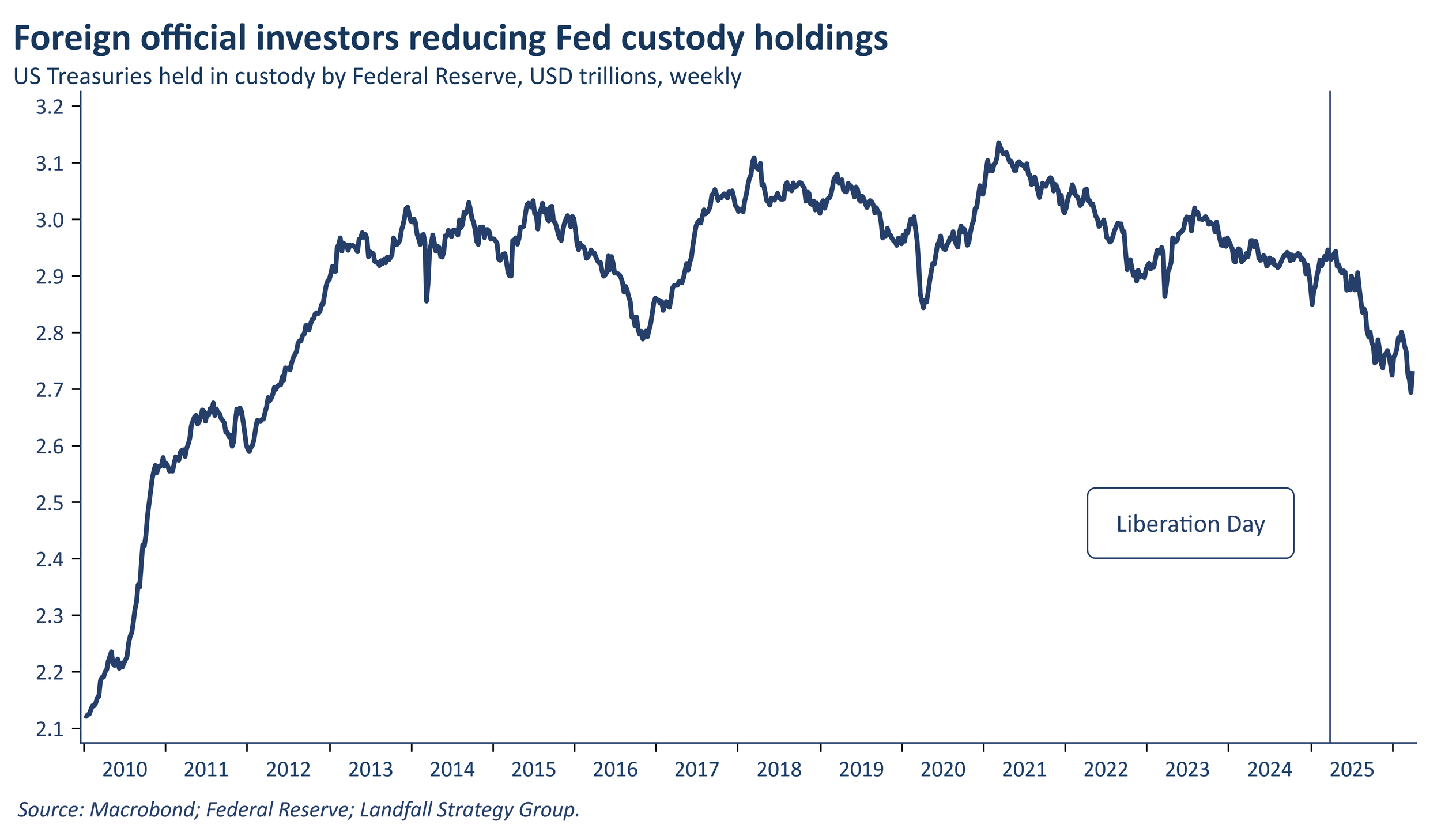

Headline foreign capital flows into the US remained steady through 2025, although there are some recent signs of softness in foreign demand for Treasuries, some institutional investor capital reallocation, and an increased risk premium being priced into US assets in response to Trump Administration decision-making and rhetoric. Looking forward, reduced capital flows from Europe, Asia, and the Gulf is likely on reduced current account surpluses. This will likely be reinforced by the Iran conflict.

USD centrality will be increasingly contested. The USD weakened by ~10% last year, and has not rallied as would historically be expected over the past month: the USD is no longer an unambiguous safe haven. The consensus view is that reserve currency status is sticky, and that changes in reserve currency status occur very gradually over horizons of decades. But during periods of global economic and geopolitical regime change, more disruptive moves are plausible.

Suez moment?

Beyond the near-term economic disruption, the attacks on Iran will have profound structural economic and geopolitical consequences. My assessment is that the distribution of structural costs will be different to the initial market response, which prices the US as more resilient than Europe and Asia. In particular, the US is uncomfortably close to a Suez moment.

It was said that the British Empire was acquired ‘in a fit of absence of mind’. Perhaps US economic and geopolitical hegemony will be diminished similarly. A more diversified, fragmented, contested global economic order is emerging, markedly different than over the past 35 years.

An acceleration of this structural shift is the most consequential economic and financial impact of the Iran conflict. Firms and investors need to position accordingly.

I work with investors and corporate leadership teams through client briefings and ongoing advisory work on the implications of global economic and geopolitical regime change.

Contact: david.skilling@landfallstrategy.com

Subscribe to these notes at: https://davidskilling.substack.com/